Is your business ready for a significant change to superannuation payments?

The Australian government announced the introduction of “Payday Super” from 1 July 2026. This change means all employers will need to pay superannuation entitlements on the same day that payroll is run, not quarterly or monthly as is currently standard practice.

For many businesses, this represents a substantial shift:

If you pay wages fortnightly, you’ll make super payments up to 22 times more often

If you pay wages weekly, you’ll make super payments up to 48 times more often

The numbers tell a compelling story: at the end of June 2023, the Australian Tax Office (ATO) estimated more than A$2.2 billion of super debt was still owed by employers to employees. In FY20 alone, an estimated $3.4 billion worth of super went unpaid. Payday Super aims to close this gap and ensure Australians receive the retirement funds they’ve earned. This change will:

Give your employees greater visibility over their super payments

Provide the ATO with real-time insights into payment compliance

Create a more transparent system for tracking and managing super obligations

How Will Payday Super Affect Your Organisation?

A revealing statistic: while 40% of businesses already pay super more frequently than quarterly, the remaining 60% of Australian businesses will face substantial changes to their financial planning and payroll processes.

Administrative Challenges

For many businesses, adapting to Payday Super will create new administrative demands:

Managing up to 48 super payment transactions annually instead of just 4 (or 12 if currently paid monthly)

Ensuring super payments reach the respective super funds on time to meet the new legislation timelines

Managing and fixing past super payments due to back payments or pay adjustments driven by late timesheets

This is especially challenging for businesses with casual workforces, where fluctuating weekly hours create variable super obligations, requiring more precise tracking and calculation with each pay run.

Transparency is about to increase significantly. With Payday Super, the ATO gains unprecedented visibility into your super payment patterns. Where unpaid contributions might previously have gone unnoticed for months, the new system creates immediate visibility. For your business, this means:

Greater urgency for timely and accurate super payments

Increased risk of penalties and fines for missed or late payments

Potential need for additional admin and compliance resources

Higher stakes for maintaining precise payroll records

The margin for error narrows considerably under this new framework, putting additional pressure on already stretched financial and payroll teams.

Payday Super creates significant financial pressures beyond compliance concerns. Organizations face increased operational costs from more frequent processing, technology investments for payroll updates, and additional resources for managing precise tracking requirements.

Increased cash flow requirements as super must be paid with each payroll cycle

Higher operational costs from processing up to 48 super payments annually

Technology investments needed to update payroll systems

Reduced financial flexibility as quarterly payment strategies disappear

Most critically, traditional cash flow management practices that incorporated quarterly superannuation payments into financial planning disappear under the new system, eliminating this strategic flexibility.

Non-compliance brings further financial consequences through SG charges, employee notifications, potential legal proceedings, and costly late payment penalties.

With Payday Super approaching, many companies are looking for ways to minimise the administrative burden it brings, while maintaining employee satisfaction. There is one popular strategy that companies are increasingly adopting, that creates advantages for both company and staff:

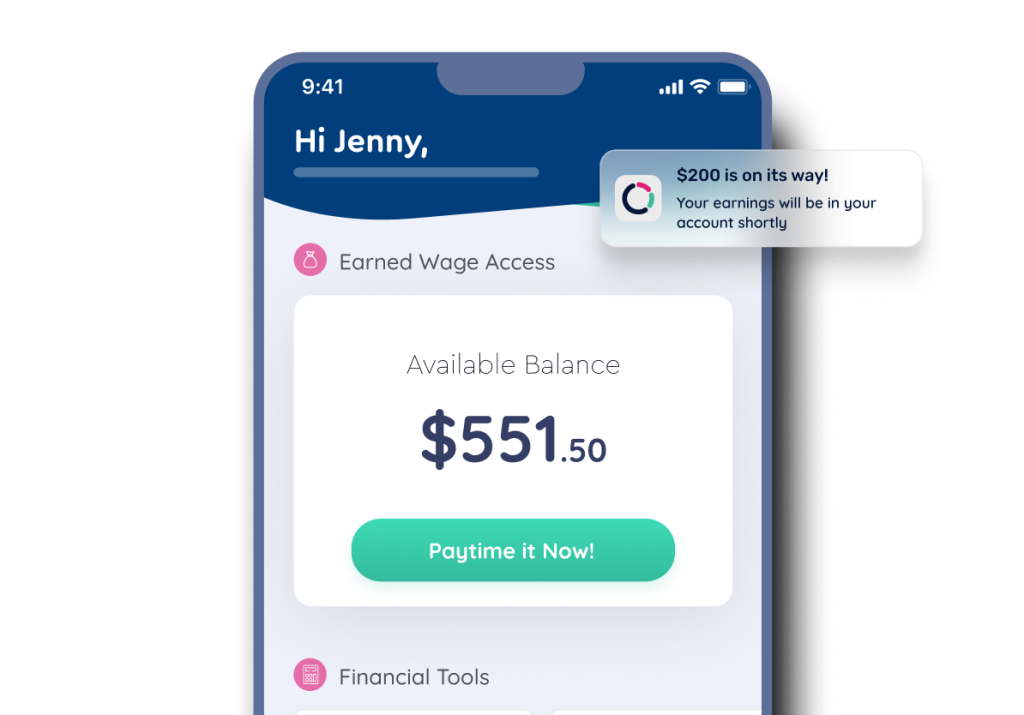

While changing pay cycles benefits your business financially, it traditionally means employees wait longer between paycheques. This is where Paytime offers a unique solution. With Paytime’s Earned Wage Access, you get the best of both worlds:

Your business gains working capital benefits through extended pay cycles

Employees receive their earned wages automatically every week

No compromise between company financial health and employee wellbeing

A true win-win that addresses a common concern among finance leaders

Changing your pay cycle frees up substantial working capital that can be reinvested into your business, as well as providing ongoing bottom line savings.

Calculate how much working

capital you can unlock

$

$

$

Days

Days

Your Estimated Working Capital Impact

Working Capital Today

$0

Working Capital (Required) With Payday Super

$0

Working Capital with Payday Super after transitioning to Fortnightly

$0

Potential Working Capital Improvement

$0

0% of monthly wages

Working Capital calculated as Current Assets - Current Liabilities

Estimated Annual Ongoing Cost Savings

Driven by processing payroll less frequently

Number of payruns saved

0 Payruns per year

Annual cost saving

$0

Source: Do You Know the True Cost of Your Payroll Operation? Aust. Payroll Assoc.

August 2014

reset

You are already optimised!

See what else Paytime can do for you.

DISCLAIMER: Please note that all the figures above and any related content about payday super are not all-inclusive and is intended for general information purposes only. It does not constitute legal or other advice. The content may not be compliant with your local employment laws. Always seek professional legal advice. Paytime expressly disclaim any representation or warranties, express or implied, including without limitation any representations or warranties of fitness for a particular purpose, accuracy, completeness and reliability. Paytime is not liable for any loss or damages arising either directly or indirectly as a result of reliance on, use of or inability to use any information provided.

We transitioned our pay cycle from weekly to fortnightly while offering Paytime to our employees. It gives our employees the flexibility to get paid on their own terms and unlocks significant working capital and administrative savings for the business

Andrew Gage Head of People and Culture at ServCo

How our clients adapted their pay cycle

Book a demo today to discover how our solution can help you adapt to Payday Super requirements while improving your financial position.

Payday Super requires employers to pay superannuation contributions at the same time as salary and wages, rather than quarterly. It takes effect on July 1, 2026, with contributions required to reach employees’ superannuation funds within 7 calendar days of payday. This legislation applies to all employers regardless of size or industry.

How will Payday Super impact business cash flow?

Businesses will need to allocate funds for super contributions with each pay cycle instead of quarterly or monthly. For businesses with weekly pay cycles, this could mean up to 52 super payments annually instead of just 4 (or 12 if you pay monthly). This increased frequency may strain cash flow.

What administrative challenges will employers face?

Employers must update payroll systems to calculate, track, and submit super payments with each pay cycle. The Small Business Superannuation Clearing House (SBSCH) will be retired by July 1, 2026, requiring businesses to transition to commercial solutions. Additionally, the ATO will have enhanced capabilities to monitor superannuation payments in near real-time through Single Touch Payroll data, making compliance monitoring more rigorous. There will also be significantly more payroll time spent on running payroll each time, in order to ensure that the superannuation amount to be paid is accurate. As companies cannot make retrospective adjustments.

How can Paytime help with Payday Super implementation?

Paytime’s Earned Wage Access solution creates a win-win scenario when changing pay cycles. Extending pay cycles benefit your business, through reduced admin burden and improved cash flows, and for Employees they can still access their earned pay automatically each week (and more if needed). This ensures company benefits don’t come at employees’ expense, as both employer and staff benefit from this approach.

What are the penalties for non-compliance with Payday Super?

Late or missed payments trigger the Superannuation Guarantee Charge (SGC), which includes the unpaid super amount, notional earnings (interest), an administrative uplift of up to 60% of the shortfall, and potential late payment penalties. While the SGC will be tax-deductible under the new system (excluding penalties and interest incurred after 28 days), the immediate financial and reputational impact can be significant.

How will Payday Super benefit employees?

Employees will see their super contributions invested sooner, with funds required to allocate contributions within 3 business days instead of 20. This more frequent investment can lead to better retirement outcomes through compounding returns. Treasury estimates that a 25-year-old median income earner could be around $6,000 or 1.5% better off at retirement due to more frequent payments. Employees will also experience greater transparency in tracking their super contributions.

What steps should my business take now to prepare for Payday Super?

Review and potentially adjust your pay cycles

Assess the impact on your cash flow management

Update payroll systems and processes

If using SBSCH, research alternative solutions

Educate your HR and finance teams

Implement robust internal controls for timely payments

Consider Earned Wage Access solutions if changing pay cycles

Even if not changing pay cycles, Earned Wage Access (EWA) is a proven financial wellbeing benefit (globally) that provides significant upside to both companies and their staff

Stay informed about legislative updates

Sources & Further Reading

Our Payday Super information is based on authoritative sources including:

For the most current information on Payday Super implementation, we recommend regularly checking the ATO website and consulting with your financial advisors.

Last updated: April 2025

Ready to Get Started?

Your payroll stays exactly the same. We handle everything else.